FOR INFORMATION ON INSURANCE SOLUTIONS CALL OR WHATSAPP +1 849-514-9838 | info@hernandezpeguero.com

Understanding Deductibles in Dominican Republic Property Insurance: A Guide for Homeowners and Expats

Learn how property insurance deductibles in the Dominican Republic affect premiums and claims for homeowners and expats in Punta Cana.

PROPERTY/HOMEOWNERS INSURANCE

HernandezPeguero.com

8/17/20252 min read

When shopping for property insurance in the Dominican Republic, many homeowners—especially expats in areas like Punta Cana—focus on coverage limits and premiums. But one factor that can significantly affect both your claim payout and your annual cost is the deductible.

Whether you’re insuring a beachfront villa, a condo in Bávaro, or a rental property, understanding how homeowners insurance deductibles work will help you choose the right balance between affordability and protection.

What Is a Deductible?

A deductible is the amount you agree to pay out-of-pocket before your insurance coverage kicks in. If you suffer a covered loss, the insurer will subtract this deductible from your claim payment.

For example:

If you have a 2% hurricane deductible on a home insured for USD $300,000, you will be responsible for the first $6,000 of hurricane-related damages before insurance covers the rest.

Why Deductibles Matter in the Dominican Republic

Deductibles directly affect your premium. In general:

Higher deductibles = Lower annual premium.

Lower deductibles = Higher annual premium, but less out-of-pocket at claim time.

In the DR, insurers often set different deductibles for different perils, especially for high-risk events like hurricanes or earthquakes.

Common Types of Deductibles in Dominican Property Insurance

Based on quotes from leading insurers like Seguros Reservas, Humano, Seguros Sura, Mapfre, and others, here’s what you can expect:

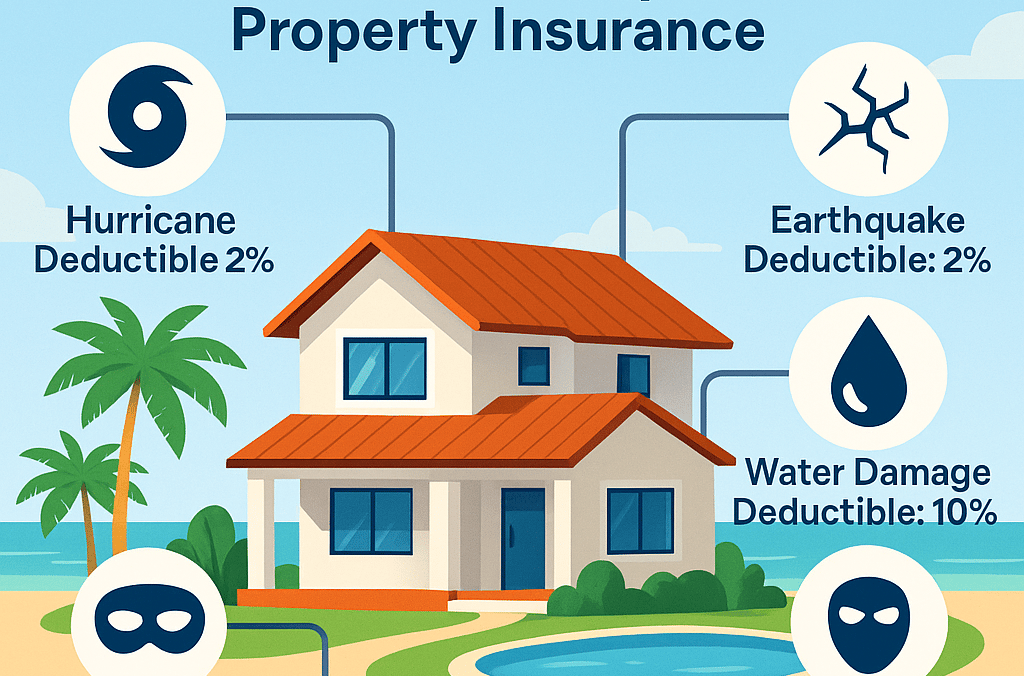

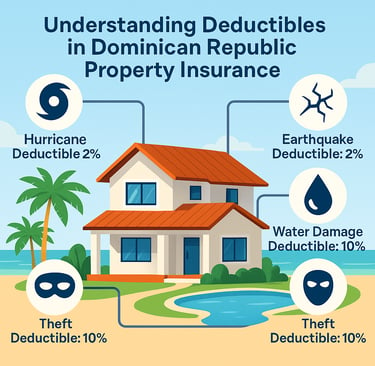

1. Hurricane, Cyclone, Tornado, Windstorm

Usually expressed as a percentage of the insured value (often 2%).

Example: A villa insured for USD $239,000 with a 2% hurricane deductible means you cover the first USD $4,780 in hurricane damages.

2. Earthquake / Tremor

Also commonly set at 2% of the insured value.

Ensures that small tremor-related cracks or cosmetic damage are not claimed for minor repairs.

3. Accidental Water Damage

Often a 10–15% deductible of the loss amount, with a minimum fixed amount (e.g., USD $150 or $250).

Applies to unexpected leaks or burst pipes, not hurricane-related water entry.

4. Theft / Burglary

Typically 10% of the loss with a minimum dollar amount.

Higher deductibles discourage small claims for minor theft.

5. Motin, Vandalism, Malicious Damage

Deductibles can be 10–15% of the loss with a set minimum.

6. Machinery Breakdown / Electronic Equipment

Commonly 15% of the loss with a fixed minimum.

Covers internal damage to household systems or electronics.

How Deductibles Affect Premiums

A lower deductible means the insurer takes on more risk—so they charge you a higher premium. If you’re a cash-flow-conscious buyer who can afford to pay more out-of-pocket in a worst-case scenario, opting for higher deductibles can significantly reduce your annual cost.

Special Considerations for Expats in Punta Cana and Coastal Areas

Hurricane Exposure: Properties near the coast almost always carry a percentage-based deductible for hurricanes and floods.

Earthquake Zone: The Dominican Republic is in a seismically active area; earthquake deductibles are standard in all policies.

Rental Properties: If you rent out your property, make sure you can handle the deductible quickly—delays in repairs can also mean loss of rental income.

Why Choose Hernández Peguero Insurance Brokers?

At Hernández Peguero, we work with top insurers in the Dominican Republic—Seguros Reservas, Humano, Seguros Sura, Mapfre, La Colonial, General de Seguros, Universal—to give you side-by-side comparisons of coverage, premiums, and deductibles.

We help you:

Understand how each deductible will affect your claims and your budget.

Negotiate payment terms, including interest-free installments or upfront payment discounts.

Ensure you get the right coverage for hurricanes, earthquakes, theft, and more.

Ready to Get a Quote?

Whether you’re a Dominican resident or an expat buying in Punta Cana, Bávaro, or anywhere in the country, we can guide you to the right balance of deductible and premium.

📞 Call/WhatsApp: +1 (849)518-9838

📧 Email: info@hernandezpeguero.com

🌐 Website: www.hernandezpeguero.com

Hernandez Peguero

Your trusted partner for comprehensive insurance solutions.

Broker

Coverage

© 2024. All rights reserved.