FOR INFORMATION ON INSURANCE SOLUTIONS CALL OR WHATSAPP +1 849-514-9838 | info@hernandezpeguero.com

Umbrella Liability in the Dominican Republic (2025): Extra Protection for Expats & Hosts

Driving, hosting or owning a high‑value condo in the DR? Learn how an umbrella policy adds US$1M+ in extra liability above home, auto and STR coverage—and how to qualify.

LIABILITY INSURANCE

HernandezPeguero.com

10/13/20255 min read

Umbrella Liability for Expats & Hosts in the Dominican Republic: When Your Limits Aren’t Enough

Own a condo in Punta Cana, drive regularly in Santo Domingo, or host guests in Las Terrenas? One serious incident can exceed standard policy limits. A personal umbrella policy—also called excess liability—adds a higher layer of protection over your existing home, auto, and short‑term rental (STR) coverage, often for a reasonable premium.

Below, we explain how umbrellas work in the Dominican Republic, who needs one, typical limits, claim scenarios, and how to qualify through a local broker.

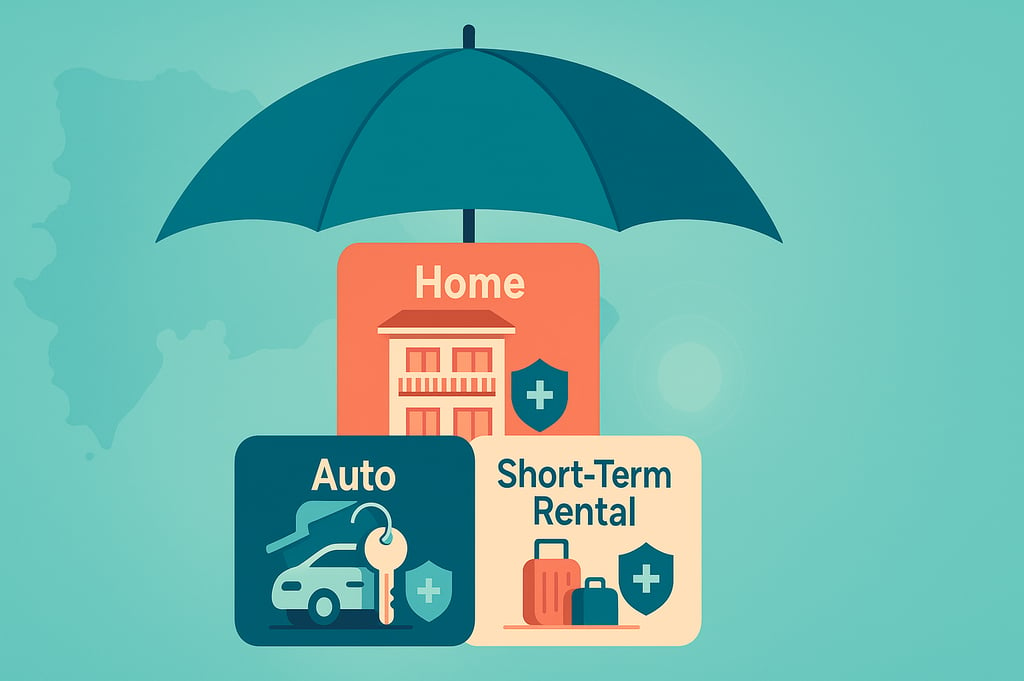

What an Umbrella Policy Actually Does

Think of umbrella insurance as a second story built on top of your base policies:

Activates after your home/condo and auto liability limits are exhausted.

May extend to personal‑injury offenses (e.g., libel/slander) depending on wording.

Can sit above landlord/STR liability (with the right endorsements and disclosures).

An umbrella does not replace base policies. Insurers require minimum underlying limits on each policy. If those are too low, the umbrella may not respond.

Related reads on our site:

DR auto basics—“Seguro de Ley vs Full”: Car Insurance in Punta Cana: Full Coverage vs. Seguro de Ley

Property/condo core coverage: Property Insurance in the Dominican Republic and our service page: Property Insurance Services

Who Should Consider an Umbrella Policy in the DR?

Condo/Villa Owners with Meaningful Assets

Entertain guests, hire contractors, or maintain staff? A severe injury can breach standard personal‑liability limits. Multiple properties or high‑value contents amplify the need.Frequent Drivers or Families with Teen Drivers

A serious collision on the Coral Highway involving multiple third parties can quickly exhaust base auto liability limits.Short‑Term Rental (STR) Hosts

Hosting in Punta Cana/Cap Cana, Las Terrenas or the Colonial Zone? Balcony, pool and stair injuries—or damage to neighbors—can escalate fast. Platform guarantees are not a substitute for real liability coverage.Public‑Facing Professionals

Business owners, creators, or community leaders sometimes add umbrellas for extra protection against personal‑injury allegations (check wording/exclusions).

If you’re unsure whether your current limits are enough, start with a quick audit of your base policies. We can review your home, auto, and travel coverage and identify gaps: Contact Us.

Typical Limits & Pricing Basics

Umbrellas are commonly issued in US$1M increments, with higher layers available. Pricing depends on:

Residences/vehicles insured

Driving and claims history

Pools, pets, watercraft, or STR exposure

Underlying limits (higher base limits can improve eligibility and price)

Many clients find the cost per additional million attractive compared to the protection gained.

Real‑World Scenarios Where Umbrella Matters

Multi‑vehicle auto injury: You’re at fault on the Autopista del Coral. Medical bills and lost wages for multiple claimants surpass your auto liability limit. The umbrella can address the excess—protecting personal assets.

Guest injury at a rental: A balcony slip requires surgery and rehab for a guest at your STR. If your rental‑liability policy responds but hits its limit, an eligible umbrella can help cover the shortfall.

Contractor accident at home: A worker is seriously injured during a renovation. Even if the contractor has coverage, disputes arise and your personal liability is implicated. The umbrella provides a higher ceiling while liability is assessed.

How Umbrellas Interact with DR Policies

Home/Condo → Umbrella

Start with strong personal‑liability limits on your homeowners/condo policy. See: Homeowners Insurance in the DR and Property Insurance Services. Confirm premises liability, medical payments to others, and host/renter endorsements if you list the property.Auto → Umbrella

Seguro de Ley is mandatory but provides low limits for severe incidents. Many drivers upgrade to Full with higher liability. Review: Car Insurance in Punta Cana: Full Coverage vs. Seguro de Ley. Umbrellas require minimum underlying liability; your auto policy must meet or exceed those to qualify.Short‑Term Rentals → Umbrella

Some carriers extend umbrellas over landlord/STR liability (subject to underwriting). Others require specific endorsements or exclude business‑related exposures. If you have multiple listings or a property‑management company, disclose fully when applying.

Underwriting Checklist: What You’ll Likely Need

Proof of underlying policies & limits (home/condo, auto, STR where applicable)

Loss/claims history for the past 3–5 years

Property details (pools, pets, security, staff)

Driver information and motor‑vehicle records (if applicable)

Ownership structure (personal name, SRL, trust)

A local broker coordinates submissions, aligns underlying limits, and negotiates wording.

Common Exclusions & Pitfalls

Business activities beyond incidental rentals (may require a commercial umbrella)

Professional liability (errors & omissions is separate)

Watercraft/ATVs unless scheduled

Intentional acts

Underlying‑limit gaps (falling below required minimums can void umbrella response)

Pro tip: Align renewal dates for home, auto, STR and umbrella so you don’t accidentally drop below required limits mid‑term.

How to Choose the Right Umbrella in the DR (Step‑by‑Step)

Map your exposures: residences, vehicles, rentals, activities with third‑party contact.

Set a target limit: Common start US$25K - 100K; scale with assets/income and risk tolerance.

Tune base policies: Lift home/condo and auto liability to the minimum underlying limits required by umbrella carriers. Also review property deductibles: Understanding Deductibles in DR Property Insurance.

Compare carriers & wording: Some are broader on personal‑injury; others narrow. Ask us for a side‑by‑side comparison.

Confirm STR treatment: Determine if covered, needs endorsement, or requires a different structure—keep platform terms and PM agreements handy.

Bundle smartly: Placing home, auto, STR and umbrella with aligned insurers can reduce gaps and speed claims.

FAQs

Is an umbrella mandatory in the Dominican Republic?

No. It’s optional—but valuable for families, expats and hosts who could face high liability claims.

Will travel insurance replace an umbrella?

No. Travel insurance focuses on medical, evacuation, trip cancellation and baggage. For travelers, see our guides: Travel Insurance—Complete Guide and our Travel Insurance service page.

Can I get an umbrella if my auto is only on Seguro de Ley?

In some cases. Most insurers require higher underlying auto liability. We can show options to upgrade.

What if I own through an SRL or trust?

Tell your broker; ownership affects how the umbrella is written and who is an insured.

Are legal defense costs included?

Often yes, but confirm whether defense is inside or outside the limit and the duty‑to‑defend clause.

Get Covered the Right Way

A well‑structured umbrella provides confidence that a single claim won’t upend your finances. The key is coordinating proper underlying limits, accurate disclosures and clear wording that matches how you live, drive and host in the DR.

For one‑on‑one help, start here:

External resources to consult (optional)

Why Choose Hernández Peguero Insurance Brokers?

We’re a bilingual, DR‑based brokerage serving expats, locals, homeowners and hosts across Punta Cana, Santo Domingo and beyond. For umbrella policies, we:

Right‑size your limits to match your assets, driving profile and hosting activity.

Coordinate underlying policies (home/condo, auto, STR) so the umbrella responds when you need it.

Compare carriers & wordings, highlighting STR‑specific endorsements where applicable.

Support you at claim time, coordinating with base policies to avoid gaps and delays.

Ready to Get a Quote?

Protect your Dominican Republic life with robust liability coverage.

👉 Contact us now:

Phone / WhatsApp: +1 849‑514‑9838

Email: info@hernandezpeguero.com

Website: www.hernandezpeguero.com

We’ll guide you to the best plan for your needs so you can enjoy your home, driving and hosting with total peace of mind.

Hernandez Peguero

Your trusted partner for comprehensive insurance solutions.

Broker

Coverage

© 2024. All rights reserved.